Who Captures Liverpool Street? A Political Economy of Network Rail & ACME

Part III: Value Capture, Governance, and the Station First Alternative

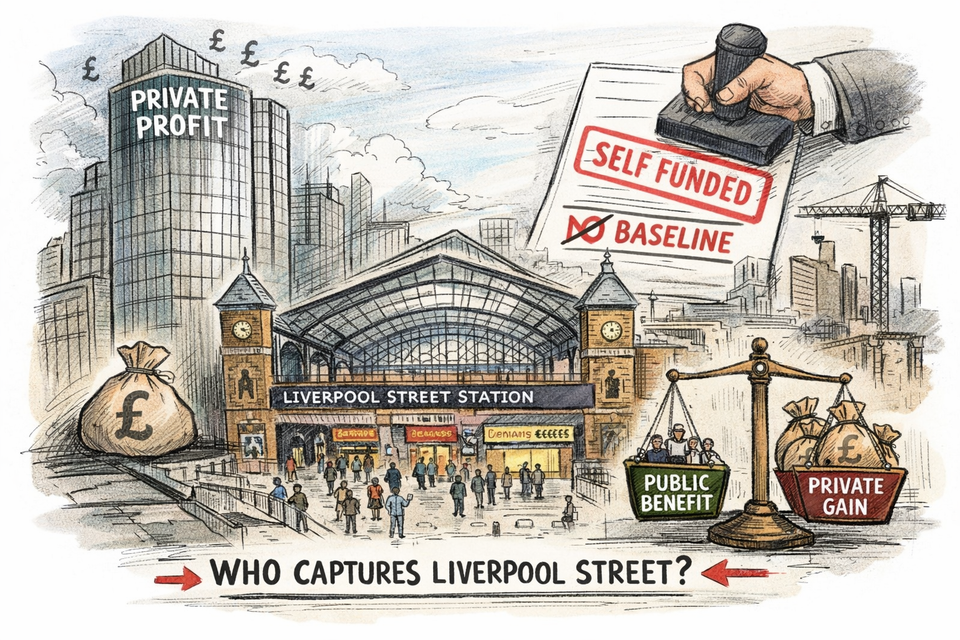

Liverpool Street is not merely a station in need of repair. It is a public node that generates value, 94.5 million passengers in 2023 moving through a 5.6 hectare estate held largely freehold by Network Rail and TfL. In places like this, an old question returns in a new form. Who captures the uplift created by public infrastructure, those who use it, or those who own the air above it.

Parts I and II of this series showed the technique by which a choice is made to look like physics. Bundle the station works to a commercial envelope. Declare the envelope minimum necessary. Keep the baseline that would allow comparison off the table. Part III does three things. It puts value capture into hard numbers. It names the governance structure that decides who gets what. And it sets out a station first alternative, not as nostalgia, but as the missing test of public reason.

1. The value machine in plain figures

The proposed development is described as a station upgrade. But the financial logic runs through the over station development, 958,687 sq ft GIA of offices over 19 storeys. This is coupled to a reconfigured retail offer, modelled in the viability appraisal as 119,229 sq ft GIA station retail.

When the numbers are laid out, something politically decisive appears.

BNP Paribas Real Estate, commissioned to review the Financial Viability Assessment, reproduces the Applicant’s split of value generation and it is revealing. In the present day appraisal outputs, station retail generates £197.5m residual land value while the office generates £44.2m, against station improvement works costs of £419.58m, leaving a large deficit.

So the office tower is presented as the enabling engine, but the appraisal itself shows the station’s retail income stream doing the heavy lifting. This is not a small technicality. It is the political economy of a station. Captive footfall is monetisable. The question is who owns the monetisation.

Now add the next layer, the layer that governance prefers to speak about softly.

JLL’s appraisal adopts a specific instrument. Station retail and advertising are assumed to be sold by way of an income strip, subject to Network Rail taking an overriding lease for 50 years and the ability to buy the interest back for £1 at the end. This is a classic asset economy move. Pull future income forward as capital today. The station becomes a yield stream packaged for transaction.

That is value capture in its raw form. Not benefit, but conversion. Public throughput translated into private finance.

2. Governance is the distribution: who gets the upside

The City is told, repeatedly, that the scheme is self funded. But self funded is not the same as public value protected. It can mean public leverage surrendered in exchange for a package of works whose scope and cost the public cannot independently benchmark against alternatives.

Consider the viability posture.

JLL state that the Applicant instructed them to assume the Benchmark Land Value is zero, £0, and they call this reasonable. BNP endorses the same position in principle. Yet this £0 assumption has an institutional consequence. It treats the airspace as a kind of moral commons, available to be monetised without a public price, while the public is asked to accept heritage loss and massing as the cost of funding.

But BNP also names the more important point. JLL structure the appraisal as though a third party developer manages the station works, the retail, and the office, and would retain the profits. BNP call this unrealistic, noting Network Rail’s direct management of other major station reconstructions and the likelihood of a JV with profit share.

Here the veil lifts. If a third party retains the profits, value leaks. If Network Rail takes the developer role, the profit becomes relevant to funding the station works. BNP quantify this explicitly. Under the JLL structure, the base case shows developer profit of £171.75m for the office. If Network Rail develops the office itself, it would receive that return and it would address the deficit. BNP also identify potential profit of £40.12m for the retail development.

This is governance as distribution. It tells us the real question the committee rarely asks in public.

Is the City approving a scheme that cross funds station works, or approving a scheme that creates profits and then chooses, by structure, how much of those profits are allowed to count as funding.

In other words, the same building can produce very different viability stories depending on who controls delivery and who captures the developer return.

3. The decade long lock in

The project timeline is not a footnote. It is governance by duration.

BNP reproduce the applicant’s programme assumptions. Lead in from Jan 2025 to Dec 2027, pre construction Dec 2027 to Dec 2028, enabling works Dec 2028 to Dec 2032, OSD construction Jan 2033 to May 2036, with sale events in March 2037. The Planning Statement summarises the arc similarly. Demolition and construction Q1 2029 to Q2 2036, station works Q2 2029 to Q4 2033, OSD construction Autumn 2031 to Q3 2036, with the station remaining operational throughout.

A long programme creates a politics of sunk cost. Once begun, the project becomes harder to question. The City absorbs disruption and risk for years while the financial logic, office yield above a station, hardens into precedent.

That is why the missing baseline is not an academic complaint. It is the difference between a public decision and a managed inevitability.

4. The station first alternative: what the documents already admit

Defenders of the scheme speak as though there were no other way. But the application documentation itself records alternative pathways.

The Planning Statement describes an optioneering exercise in which options include refurbishment led routes without an OSD and routes with new office construction. It lists, among those taken forward for detailed assessment:

Option B: major refurbishment of LSS, full retention of 50 Liverpool Street, new concourse, no Ticket Hall B intervention and no OSD

Option C: major refurbishment, demolition of 50 Liverpool Street, new concourse, Ticket Hall B intervention, no OSD

Option E: major refurbishment with Ticket Hall intervention and a 16 storey OSD

Option G: major refurbishment, full demolition of 50 Liverpool Street, Ticket Hall B intervention, new build 16 storey OSD

AECOM’s conclusion, as reported, is that Option G is preferred and that it is the only option that will deliver all of the public benefits. This is the line that closes the argument.

But note what is missing from public view. A station first minimum baseline with a cost plan, a deliverability path, and a defined scope, set alongside the OSD options on the same footing. The existence of Options B and C proves the point. The question is not whether alternatives exist. The question is whether they were allowed to become democratically legible.

A baseline is not an option. It is the minimum public settlement. The least harmful set of works that delivers operational necessity, capacity, step free access, safety, legibility, without treating an office tower as the precondition of civic repair.

Without that baseline, “only option” is not a conclusion reached by comparison. It is a label used to close the comparison down.

5. What value capture would look like in an honest settlement

If Liverpool Street is a value generating public node, then the City’s duty is not merely to approve benefits. It is to govern the distribution of uplift so that the gains created by public infrastructure return to the public on enforceable terms.

There are at least five mechanisms an authority serious about value capture would put on the table before granting permission for a project of this kind.

First, publish the station first minimum baseline. Scope, cost, and programme, separating necessity from enhancement, so minimum necessary becomes testable rather than asserted.

Second, require a transparent alternatives appraisal. Not one scheme and a story, but multiple schemes costed and compared, including Options B and C explicitly and publicly.

Third, make the delivery structure a public condition. Because, as BNP show, the viability story changes materially depending on whether profit leaks to a third party or is captured by Network Rail or a JV and applied to station works.

Fourth, tie value capture to the station’s revenue realities. The Applicant’s own appraisal outputs show retail generating far more residual value than office in the present day case. That should trigger governance questions about retail rent setting, revenue participation, and long term public return, especially where retail income is packaged as an income strip.

Fifth, enforce public benefit as contract, not narrative. When the project is programmed across 2029 to 2036 with major phasing and disruption, the City should bind public benefits to enforceable deliverables, triggers, and remedies, not merely to goodwill over a decade.

These measures are not radical. They are simply the basic tools any public authority should use when a public transport asset is being turned into a revenue machine and used to justify a major private development deal.

6. Conclusion: public benefit without a baseline is a licence to transfer

Liverpool Street is being rebuilt in the image of the age. The station as civic necessity, the airspace as commercial opportunity, and the planning process as the ceremony that converts one into the other.

The documents already show what must be faced. The funding story rests on monetisation. 958,687 sq ft of offices, an expanded retail engine, and a financial instrument that sells future station income forward under a 50 year structure with a £1 buy back. The viability framing is not settled science. It is governance by assumption, £0 land value, structured delivery, and competing accounts of profit and leakage. The alternatives exist in outline, yet the station first minimum was never allowed to become the public’s reference point.

So we return to the series question, now sharpened by the numbers.

Who captures Liverpool Street.

If the answer is the market, by default, then public benefit is not a balance. It is a permission slip.

And if the answer is the public, by right, then the first act of democratic repair is simple. Publish the station first minimum baseline, and let the city see the choice it is being asked to make.

Editorial Note

This article is published in good faith as commentary and analysis on a matter of public interest: the redevelopment of Liverpool Street Station and the political economic rationale offered for the associated over station office development.

It draws on publicly available planning documents submitted in connection with the Liverpool Street Station application, including viability and circular economy materials prepared for or on behalf of Network Rail Infrastructure Limited and reviews commissioned by the City of London Corporation.

All interpretation and argument are the author’s own, prepared with regard to principles of accuracy, fairness, and responsible journalism consistent with the National Union of Journalists’ Code of Conduct and IPSO Editors’ Code.